By Eric Mersch

The Remaining Performance Obligation (RPO) reporting requirement arose from adopting ASC 606. This SaaS metric is defined as the sum of Deferred Revenue and Backlog. Deferred Revenue for SaaS companies is the non-cancellable contractual obligation to deliver the SaaS product for the period invoiced. The term Backlog refers to future non-cancellable contractual obligations. A derivative of this metric, called the Current Remaining Performance Obligation, or cRPO, refers to the service obligations over the next twelve months from the reporting period. Public companies were slow to incorporate the RPO metrics in their investor communications, but their use is now widespread.

Remaining Performance Obligation (RPO) – the sum of Deferred Revenue and Backlog.

Current Remaining Performance Obligation (cRPO) – the sum of Deferred Revenue and Backlog the company must deliver over the next twelve months.

The RPO Reporting Requirement

The reporting guidance on Remaining Performance Obligations originated with the official adoption of Accounting Standards Update No. 2014-09, Accounting Standards Codification (ASC) number 606: “Revenue From Contracts With Customers,” which was required for public companies with annual periods that began after December 15th, 2017.

A company’s Remaining Performance Obligation (RPO) represents the total future performance obligations arising from contractual relationships. More specifically, RPO is the sum of the invoiced amount and the future amounts not yet invoiced for a contract with a customer. The former amount resides on the balance sheet as Deferred Revenue and has always been reported as GAAP requires. The latter obligation, called Backlog, makes up the non-invoiced amount of the Total Contract Value metric. Thus, RPO equals the sum of Deferred Revenue and Backlog.

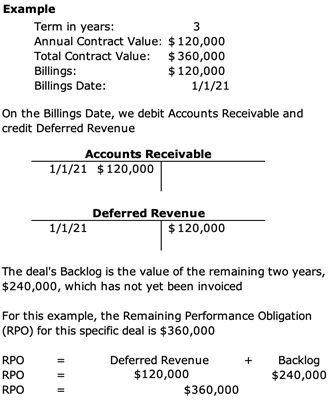

Now, let’s us look at an example. We will use an for our example because these companies typically have contract terms greater than one year’s duration. In this case, assume that our theoretical company closes a three-year SaaS deal with an average Annual Contract Value (ACV) of $120,000. The contract requires a one-year upfront payment. On the Billings date, the company debits Accounts Receivable (AR) and credits Deferred Revenue (DR) for $120,000. On the payment date, the company credits AR and debits Cash for the $120,000 payment. At this point, the company has a contractual obligation to deliver the SaaS product for three years. But only the economic activity of the first year is accounted for in its financials. The Backlog, which is the dollar value of the remaining two years of the contract, is the sum of the contract’s second two years, or $240,000. The Backlog value is not recorded on the balance sheet. The Remaining Performance Obligation is the sum of the Deferred Revenue ($120,000) and the Backlog ($240,000), or $360,000.

Venture-backed companies have long tracked this dynamic, though not with RPO. We use average Total Contract Value (TCV) and the ratio between TCV and ACV as metrics to measure future revenue opportunity. In the example above, TCV is the value of the three-year deal or $360,000 and the TCV/ACV metric is 3.0.

As we saw in the example above, RPO is not a GAAP number and, therefore, does not appear on the balance sheet. Instead, companies report it in the Revenue from Contracts with Customers section of the public filings. The amounts are reported in millions, so not at the same level of detail as GAAP numbers. Companies often report RPO by revenue line item. For example, the work management and collaboration software provider Smartsheet breaks out RPO from subscription and from professional services. Additionally, companies report the RPO amount that it is expected to be recognized in the next 12 months and this is called the Current Remaining Performance Obligation, cRPO.

The Remaining Performance Obligation as a Replacement to Billings

Most public SaaS companies include information on the Billings associated with the period. Billings is a non-GAAP metric defined as the dollar value of the New or Renewal Subscription Bookings amount invoiced on the date dictated by the contract terms, i.e., the Billings Date. The purpose of Billings as a metric is to provide an indication of future revenue. If using Billings as a key metric, the company will provide a reconciliation of Billings to Revenue using the change in Deferred Revenue. For example, cybersecurity company Tenable Holdings, Inc. (NASDAQ: TENB) uses a metric it calls Calculated Billings and uses the change in Deferred Revenue to reconcile this non-GAAP metric to GAAP revenue.

However, some investors find the Billings metric confusing because of the reconciliation to revenue. RPO potentially solves this issue because it better captures all future obligations or those for the next twelve months using cRPO. Tenable has joined other companies in report RPO in addition to Billings. In its 10-K filing for the fiscal year ending December 31, 2019, Tenable added this section on RPO: Remaining Performance Obligations: At December 31, 2019, the future estimated revenue related to unsatisfied performance obligations was $367.3 million, with approximately 75% expected to be recognized as revenue over the succeeding twelve months, and the remainder expected to be recognized over the four years thereafter.[1]

Tenable’s shift towards RPO reporting shows that RPO could at the very least augment Billings if not fully replace it.

Splunk was an early adopted of the Remaining Performance Obligation

One of the early SaaS adopters was Splunk Inc., which implemented ASC 606 on February 1, 2018, and provides a good reference for RPO. For that first fiscal year following RPO adoption, Splunk reported Total Revenues of $1.80B, Deferred Revenue of $0.88B and RPO of $1.26B. For the following fiscal year, Splunk reported Total Revenues of $2.36B, Deferred Revenue of $1.00B and RPO of $1.80B. Year-over-year growth in RPO was 43% and this exceeded the growth in Total Revenues by 12 points. Since RPO serves as a proxy for future revenue, the RPO growth rate provides a leading indicator of growth. In Splunk’s case, the RPO growth indicates that the company will show Total Revenue growth in fiscal year 2021.

Two years later, for the fiscal year ending January 31, 2020, Splunk still reported on RPO, but dropped billings as a metric. This suggests that investors are beginning to find RPO a more valuable reporting metric than Billings.

Current Remaining Performance Obligation (cRPO)

Okta, Inc., a cybersecurity and identity solutions company, recently adopted cRPO as a metric for public reporting. The addition of cRPO appears in its first quarter fiscal year 2023 financial results. Indeed, Okta uses cRPO as one of its four key non-GAAP metrics. While Okta still reports Billings, actually Calculated Billings, it does not include a Billings to Revenue reconciliation.

Summary

The Remaining Performance Obligation (RPO) metric is a valuable key performance indicator for the momentum of the business. Since its introduction in 2018, the use of RPO has gained significant traction. And, now we are seeing RPO derivatives such as cRPO. As an operator, you would be wise to use RPO as a key performance indicator.

Eric Mersch

Eric Mersch has over 20 years of executive finance experience including twice serving in public company Chief Financial Officer roles. Eric is an equity partner at FLG Partners where he works as an Interim CFO to venture-backed SaaS and subscription companies, specializing in Strategy and Operations, Strategic Planning, Equity &…Read More